PyroGenesis Announces 2024 Second Quarter Results

Gross profit: $1.12 million

Total revenue (Q2): $3.93 million, +29.6% year-over-year

Backlog: $29.8 million

MONTREAL, Aug. 06, 2024 (GLOBE NEWSWIRE) -- PyroGenesis Canada Inc. (http://pyrogenesis.com) (TSX: PYR) (OTCQX: PYRGF) (FRA: 8PY), a high-tech company (the “Company” or “PyroGenesis”) that designs, develops, manufactures and commercializes advanced plasma processes and sustainable solutions which are geared to reduce greenhouse gases (GHG) and address environmental pollutants, is pleased to announce its financial and operational results for the second quarter ended June 30th, 2024.

“With Q2’s strong earnings, PyroGenesis continues its string of positive results reflecting growing industry momentum and customer interest, together with corporate commitment to optimizing expenditures and processes. After posting a three-year low revenue mark back in Q1 2023, we now have posted 5 consecutive quarters of revenue improvement, with four of those quarters, including this most recent, surpassing the previous quarter’s revenue,” said P. Peter Pascali, President and CEO of PyroGenesis.

“The collection of key receivables whose payment timelines were strategically extended, together with a cost reduction program, and the meeting of significant project milestones, resulted in us posting these results. Second-half trends, including the post-quarter end announcement of a large land-based waste-to-energy system design and potential development contract, provides me with the confidence that PyroGenesis will continue to distinguish itself in the industrial decarbonization and electrification arena well beyond 2024.”

KEY Q2 2024 FINANCIAL HIGHLIGHTS

- Revenue of $3.93 million, up 29.6% year-over-year vs. Q2 2023

- An increase of 13% vs. Q1 2024

- 3rd best Q2 revenue in Company’s history

- Backlog of signed and/or awarded contracts of $29.8 million as at August 6, 2024

- Gross margin of 29%

- Net income of $1.4 million, earnings per share of $0.01

SUBSEQUENT EVENTS

- Post quarter end, in July 2024 [news release dated July 22, 2024], the Company announced the closing of a $2.8 million non-brokered private placement consisting of the issuance and sale of 3,505,750 units at a price of $0.80 per unit, for gross proceeds of $2,804,600. Each unit consists if one common share of PyroGenesis, and one common share purchase warrant, entitling the holder to purchase one common share at a price of $1.20 during the twelve months following the closing date of the private placement. Among the subscribers, the CEO and their related parties directly or indirectly purchased in excess of $1 million of this private placement.

- Post quarter end, in July 2024 [news release dated July 03, 2024], the Company announced that up to 4,107,850 common share purchase warrants will be amended such that the exercise price would be reduced to $0.75 per share provided that if the closing price of the common shares exceeds $0.9375 (such amount being 125% of $0.75) over any 5 consecutive trading days, the Company will be entitled to accelerate the expiry date of the warrants to the date that is 30 days following that notice of such acceleration is provided.

- Post quarter end, in July, the Company’s client, HPQ Silicon Inc., announced [news release dated July 30th] the start of commissioning of the Fumed Silica Reactor (FSR) pilot plant for which the Company has been designing, engineering, and constructing a proprietary technology to convert quartz (SiO2) into fumed silica (also known as pyrogenic silica) in a single and eco-friendly step while eliminating the use of harmful chemicals generated by conventional methods. The FSR, if successful, could provide a groundbreaking contribution to the repatriation of silica production to North America. Fumed silica is a moisture-absorbing white microstructure powder with high surface area and low bulk density. Used most often as a thickening agent, anti-caking agent, and stabilizer to improve the texture and consistency of products, the commercial applications of fumed silica can be found in many industries across thousands of product lines, including – but not limited to – personal care, powdered food, pharmaceuticals, agriculture (food & feed), adhesives, paints, sealants, construction, batteries and automotive.

- Post quarter end, the Company announced [news release dated July 29, 2024] the signing of a contract for a land-based waste-to-energy system to a European entity, to transform municipal solid waste into both energy and chemical products. The contract was announced as two phased: phase 1 is a signed $2 million contract for a conceptual and preliminary design phase; phase 2 is the construction and delivery of a final system. Phase 1 is expected to be completed in 2025. Phase 2 is dependent on the client obtaining the required financing and the negotiation of terms and conditions. As noted in the news release, the potential value for this contract grew from approximately $25-$30 million to between $120-160 million, with final decision based on the results of the phase one project, which is scheduled for completion in Q3 2025.

Q2 2024 PRODUCTION AND SALES HIGHLIGHTS

The information below represents highlights from the past quarter for each of the Company’s main business verticals.

Q2 2024 continued the positive revenue growth trend that began in Q2 2023. Q2 2024 marks the 5th straight quarter of revenue improvement compared to the low revenue mark of Q1 2023, with four of those five quarters – including Q2 2024 – surpassing the previous quarter’s revenues.

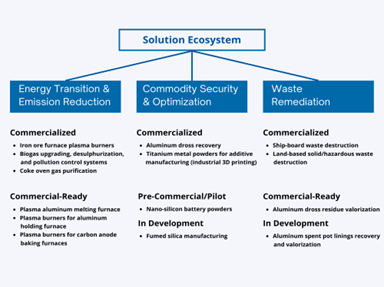

The Company operates within three verticals that align with economic drivers that are key to global heavy industry:

- Energy Transition & Emission Reduction:

- fuel switching – utilizing the Company’s all-electric plasma torches and biogas upgrading technology to help heavy industry reduce fossil fuel use and greenhouse gas emissions,

- Commodity Security & Optimization:

- recovery of viable metals – and optimization of production methods/processes geared to increase output, maximize raw materials and improve availability of critical minerals,

- Waste Remediation:

- safe destruction of hazardous materials – and the recovery and valorization of underlying substances such as chemicals and minerals.

Within each vertical the Company offers solutions at different stages of commercialization.

Energy Transition & Emission Reduction

- In April, the Company announced a signed letter of intent with global aluminum product manufacturer Constellium for large-scale plasma remelting furnaces, amid an agreement to investigate the potential replacement of fossil fuel burners in Constellium’s furnaces, following the previous completion of successful trials with PyroGenesis that occurred during 2023. With the new agreement, the two companies have agreed to implement an industrial scale aluminum remelting furnace using plasma as the heat source.

- In April, the Company announced a contract with a global mining supply company, with the agreement related to the client’s intention to examine the use of plasma in decarbonizing its cast houses. The agreement outlined both a test phase and potential on-site initiative that replaces existing fossil fuel burners with the Company’s plasma torches.

- In April, the Company announced a contract with one of the five largest global steelmakers to assess the applicability of plasma use in primary steel production, specifically during the production of direct reduced iron for use in electric arc furnaces.

- In May, the Company announced that its wholly-owned subsidiary, Pyro Green-Gas, had signed contracts with a global steel company based in India, for the development and supply of technology to desulphurize and clean the gas that is released during the creation of metallurgical coke from coal. Under the terms of these contracts, Pyro Green-Gas will provide engineering and mechanical solutions that will aid in the removal of hydrogen sulfide from coke oven gas during the coking process. The cleaned gas would then be converted into high value reusable hydrogen.

- In June, the Company announced that its wholly-owned subsidiary, Pyro Green-Gas, had signed a contract for the engineering, design, and fabrication of a thermal swing adsorption system for the dehydration of pure oxygen produced from electrolyzers at the Varennes Carbon Recycling Plant – a large biofuel production project currently under construction in Varennes, Quebec.

Commodity Security & Optimization

- In April, the Company announced the positive results of laboratory tests for its green cement project with client Progressive Planet, whereby the cement additive product known as PozPyro achieved compressive strength tests at the 7-day mark that were 45% above the target for green cement additive products. The goal of the project is to create a replacement for fly ash, used in cement as an additive, but which is in diminishing supply due to the ongoing reduction in coal-fired power plants that create fly ash. PozPyro is made using quartz silica, an abundant material.

- In April, the Company announced a contract to supply a Spanish aerospace entity with titanium metal powder produced by the Company’s NexGen™ plasma atomization system. The client is engaged in the development of advanced aeronautics technologies for the European aerospace industry, and will use the titanium powder for additive manufacturing purposes. This contract represents the first contract under the Company’s new European distribution strategy that supplies the Company’s powder direct to customers rather than via third party distributors.

- In May, the Company announced additional positive results of laboratory tests for its green cement project with client Progressive Planet, whereby the cement additive product known as PozPyro achieved compressive strength tests at the 28-day mark that were up to 99.56% above the target for green cement additive products.

- In June, the Company announced that it had cleared the final requirement to becoming an approved supplier of its titanium metal powder to a global aerospace original equipment manufacturer. The Company’s “course” cut Ti64 metal powder had met all of the necessary requirements to be added to the client’s approved supplier list, and the formal process for adding the Company to the approved supplier list has begun. The Company has been engaged in an extensive qualification process with the client lasting several years leading to this announcement.

- In June, the company announced that it had received a second signed contract with a Spanish aerospace entity for titanium metal powder produced by the Company’s NexGen™ plasma atomization system. The client is engaged in the development of advanced aeronautics technologies for the European aerospace industry, and has indicated that the Company may qualify for a long-term contract following the successful completion of this contract.

Q2 2024 FINANCIAL HIGHLIGHTS

- In April, the company announced a block sale of HPQ Silicon Inc. shares to the Company’s President and CEO, Photis Peter Pascali, for an aggregate purchase price of $661,447.50, representing a per share price of $0.175. As noted in the news release by the Company’s CFO, Andre Mainella: “This sale will bring PyroGenesis an influx of cash on favourable terms.”

- In April, the Company announced receipt of two separate milestone payments totaling $970,000 for the sale of a plasma torch system to a U.S. corporation developing a system geared to destroy perfluoroalkyl and polyfluoroalkyl substances (“PFAS”).

- In May, the Company announced receipt of $1.5 million as settlement in legal proceedings between the Company’s wholly-owned subsidiary Pyro Green-Gas and certain related persons and Gas RNG Systems Inc. and certain persons. The settlement was concluded on a no-fault basis, with all parties to the proceedings providing full and final releases.

- In June, the Company announced receipt of $4.1 million under the Drosrite™ contract with Drosrite International and its client Radian Oil and Gas, as part of an outstanding receivable under the Company’s existing $25 million Drosrite™ contract.

Q2 2024 OPERATIONAL HIGHLIGHTS

- In April, the Company announced the appointment of Mr. Paul Rajchgod to the Board of Directors as an independent member of the board.

- In May, the Company announced that it notified HPQ Silicon Inc. of its intent to exercise its option to convert its annual royalty rights into a 50% ownership of HPQ Silica Polvere Inc, a wholly owned subsidiary of HPQ Silicon Inc. HPQ Polvere’s primary initiative is the Fumed Silica Reactor (FSR) project, for which the Company has been designing, engineering, and constructing a proprietary technology to convert quartz (SiO2) into fumed silica (also known as pyrogenic silica) in a single and eco-friendly step while eliminating the use of harmful chemicals generated by conventional methods. The FSR, if successful, could provide a groundbreaking contribution to the repatriation of silica production to North America. Fumed silica is a moisture-absorbing white microstructure powder with high surface area and low bulk density. Used most often as a thickening agent, anti-caking agent, and stabilizer to improve the texture and consistency of products, the commercial applications of fumed silica can be found in many industries across thousands of product lines, including – but not limited to – personal care, powdered food, pharmaceuticals, agriculture (food & feed), adhesives, paints, sealants, construction, batteries and automotive.

FINANCIAL SUMMARY

1. Revenues

PyroGenesis recorded revenue of $3.9 million in the second quarter of 2024 (“Q2, 2024”), representing an increase of $0.9 million compared with $3.0 million recorded in the second quarter of 2023 (“Q2, 2023”). Revenue for the six-month period ended June 30, 2024, was $7.4 million, an increase of $1.8 million over revenue of $5.6 million in the same period of 2023.

Revenues recorded in the three and six-months ended June 30, 2024, were generated primarily from:

| Three months ended June 30 | Variation | Six months ended June 30 | Variation | |||||||||||

| 2024 | 2023 | 2024 vs 2023 | 2024 | 2023 | 2024 vs 2023 | |||||||||

| High purity metallurgical grade silicon & solar grade silicon from quartz (PUREVAP™) | 101,790 | 445,840 | (344,050 | ) | 496,234 | 973,439 | (477,205 | ) | ||||||

| Aluminium and zinc dross recovery (DROSRITE™) | 327,503 | 115,325 | 212,178 | 990,688 | 205,552 | 785,136 | ||||||||

| Development and support related to systems supplied to the U.S. Navy | 237,175 | 813,125 | (575,950 | ) | 1,281,609 | 1,165,228 | 116,381 | |||||||

| Torch-related products and services | 2,792,009 | 561,942 | 2,230,067 | 3,669,057 | 1,732,690 | 1,936,367 | ||||||||

| Refrigerant destruction (SPARC™) | 149,173 | 187,444 | (38,271 | ) | 251,891 | 255,292 | (3,401 | ) | ||||||

| Biogas upgrading and pollution controls | 175,959 | 618,070 | (442,111 | ) | 208,008 | 650,965 | (442,957 | ) | ||||||

| Other sales and services | 155,489 | 297,733 | (142,244 | ) | 528,008 | 647,935 | (119,927 | ) | ||||||

| Revenue | 3,939,098 | 3,039,479 | 899,619 | 7,425,495 | 5,631,101 | 1,794,394 | ||||||||

Q2, 2024 revenues increased by $0.9 million, mainly as a result of:

- PUREVAP™ related sales generated revenue of $0.1 million, a decrease of $0.3 million compared to Q2 2023 due to the completion of the project and with the successful silicon “pour” previously announced by the Company. As a result, minimal revenue was forecasted and realized in the current quarter,

- DROSRITE™ related sales increased by $0.2 million due to the increase in spare parts orders from existing clients and the increase in storage revenue and other ancillary revenue related to the DROSRITE units, at the request of the client,

- Development and support related to systems supplied to the U.S generated revenue of $0.2 million, a decrease of $0.6 million compared to Q2 2023 due to the current stage of the project, whereas, in the comparable period, significant advancement was made related to inspection, packaging and shipment of the equipment to our customer in order to move forward with installation and commissioning,

- Torch-related products and services increased by $2.2 million, due to the continued progress on the significant projects related to our 4.5MW and 1MW torch systems, and additional recurring monthly 24/7 onsite support,

- Biogas upgrading and pollution controls generated revenue of $0.2 million, a decrease of $0.4 million compared to Q2 2023 due to the decrease in project volume,

During the six-month period ended June 30, 2024, revenues varied by $1.8 million, mainly as a result of:

- PUREVAP™ related sales decreased to $0.5 million due to the completion of the project and current project phase, whereby lower revenue was expected,

- DROSRITE™ related sales increased to $0.9 million due to the increase in spare parts orders from existing clients and the increase in storage revenue and other ancillary revenue related to the DROSRITE units,

- Development and support related to systems supplied to the U.S Navy increased by $0.1 million due to the current stage of the project, whereby, in the comparable period, and beginning of 2024, significant advancement was made related to inspection, packaging and shipment of the equipment to our customer in order to move forward with installation and commissioning, in addition to the increase in awarded contracts for spare parts and engineering services from clients that are third-party suppliers of the US Navy,

- Torch-related products and services increased by $1.9 million, due to the Company providing continuous 24/7 onsite support and the significant progress related to the current ongoing torch systems projects,

- Biogas upgrading and pollution controls related sales decreased by $0.4 million due to a decrease in project volume,

As of August 6, 2024, revenue expected to be recognized in the future related to backlog of signed and/or awarded contracts is $29.8 million. Revenue will be recognized as the Company satisfies its performance obligations under long-term contracts, which is expected to occur over a maximum period of approximately 3 years.

2. Cost of Sales and Services and Gross Margins

Cost of sales and services were $2.8 million in Q2 2024, representing an increase of $0.9 million compared to $1.9 million in Q2, 2023, primarily attributable to a $1.4 million increase in direct materials which reached $1.7 million. The increase in direct materials is related to the recognition of costs from the completion of the power supplies required for the Company’s high-powered torch systems. However, the increase was offset by the decrease in employee compensation of $0.1 million reducing it to $0.8 million (three-month period ended June 30, 2023 - $0.9 million), and a decrease of $0.2 million in subcontracting (three-month period ended June 30, 2023 - $0.2 million), attributed to additional work being completed in-house and the product mix related to the cost of sales.

The gross profit for Q2, 2024 was $1.1 million or 29% of revenue compared to a similar gross profit of $1.1 million for Q2 2023, however it represents 37% of revenue. The decrease in gross margin percentage was mainly due to the increase on direct materials costs, and to the 2023 Q2 sales mix which has higher margins.

During the six-month period ended June 30, 2024, cost of sales and services were $5.5 million, an increase from $4.0 million for the same period in the prior year. The $1.6 million increase is primarily driven by a $2.0 million rise in direct materials related to the recognized costs of substantial items, namely power supplies. This increase was partially offset by the decrease in subcontracting expenses of $0.2 million attributed to additional work being completed in-house and the product mix related to the cost of sales.

The amortization of intangible assets for Q2, 2024 was $0.02 million compared to $0.2 million for Q2, 2023, and during the six-month period ended June 30, 2024, was $0.1 million compared to $0.4 million for the same period in the prior year. This expense variation relates mainly to the intangible assets in connection with the Pyro Green-Gas acquisition, which have been fully amortized by January 2024. These expenses were non-cash items, and the remaining intangible assets are composed of patents, and deferred development costs that will be amortized over the expected useful lives.

As a result of the type of contracts being executed, the nature of the project activity, as well as the composition of the cost of sales and services, the mix between labour, materials and subcontracts may be significantly different. In addition, due to the nature of these long-term contracts, the Company has not necessarily passed on to the customer, the increased cost of sales which was attributable to inflation, if any. The costs of sales and services are in line with management’s expectations and with the nature of the revenue.

3. Selling, General and Administrative Expenses

Included within Selling, General and Administrative expenses (“SG&A”) are costs associated with corporate administration, business development, project proposals, operations administration, investor relations and employee training.

SG&A expenses for the second quarter of 2024 amounted to $0.2 million, reflecting a significant decrease of $6.2 million from Q2 2023. This reduction is primarily attributed to several key factors. The expected credit loss and bad debt experienced a substantial decrease of $5.2 million, primarily due to a $4.1 million payment received on a previously provisioned outstanding receivable. This payment led to a reversal of the previously recognized credit loss. Additionally, there was a decrease in the expenses following the settlement of legal proceedings involving Pyro Green-Gas and Gas RNG Systems Inc., which concluded favourably, with a $1.5 million payment. Professional fees were reduced by $0.3 million from the three-month period ended June 30, 2023, due to decreased reliance on external consultants, legal services, and other professional services. Other expenses showed a favorable variance of $0.5 million, driven by reductions in insurance expenses and marketing costs. Additionally, there was a favorable impact of $0.4 million due to changes in the foreign exchange charge on materials due to the variation of the U.S. dollar.

These decreases were partially offset by an increase in employee compensation by $0.1 million. There was also an increase of $0.2 million in office and general expenses. Moreover, there was a positive variance of $0.3 million in government grants due to higher levels of activities supported by such grants.

During the six-month period ended June 30, 2024, SG&A expenses totaled $4.8 million, a notable decrease of $9.2 million from $14.0 million for the same period in the prior year. The key factors contributing to this decrease include the expected credit loss and bad debt provision, which varied favourably by $6.2 million. This was caused mainly by the payment received from a customer whose balance was provisioned, and to higher credit loss expense recognized in Q2 2023. Employee compensation decreased by $0.3 million. Professional fees saw a significant reduction of $1.0 million due to less reliance on external consultants, legal services, and other professional services. Other expenses decreased by $0.7 million, as well, there was a favorable impact of $0.7 million on the foreign exchange charge on materials due mainly to the variation of the U.S. dollar.

Share-based compensation expense for the three and six-month periods ended June 30, 2024, was $0.3 million and $0.8 million, respectively (three and six-month periods ended June 30, 2023 - $0.7 million and $1.7 million, respectively), a decrease of $0.4 million and $1.0 million respectively, which is a non-cash item and relates mainly to 2022, and 2023 grants not repeated in 2024.

Share-based payments expenses as explained above, are non-cash expenses and are directly impacted by the vesting structure of the stock option plan whereby options vest between 10% and up to 100% on the grant date and may require an immediate recognition of that cost.

4. Depreciation on Property and Equipment

The depreciation on property and equipment for the three and six-month periods ended June 30, 2024, decreased to $0.1 million and $0.16 million, respectively, compared with $0.2 million and $0.3 million for the same periods in the prior year. The expense is comparable to the same quarters last year and the decrease is primarily due to the nature and useful lives of the property and equipment being depreciated.

5. Research and Development (“R&D”) Costs, net

During the three-months ended June 30, 2024, the Company incurred $0.3 million of R&D costs on internal projects, a decrease of $0.5 million when compared to Q2 2023. The decrease in Q2 2024 is primarily related to a decrease in employee compensation and in other expenses due to a reduction in R&D activities.

During the six-months ended June 30, 2024, the Company incurred $0.5 million of R&D costs on internal projects, a decrease of $0.6 million when compared to the same period in the prior year. The decrease is mainly due to lower levels of R&D activities in the 2024 period.

In addition to internally funded R&D projects, the Company also incurred R&D expenditures during the execution of client funded projects. These expenses are eligible for Scientific Research and Experimental Development (“SR&ED”) tax credits. SR&ED tax credits on client funded projects are applied against cost of sales and services (see “Cost of Sales” above).

6. Finance Expenses (income), net

Finance expenses for Q2 2024 totaled $0.3 million as compared with an income of $0.9 million for Q2, 2023, representing a variation of $1.3 million year-over-year. The increase in finance expenses in Q2 2024 is mainly due to the favourable $1.1 million of the revaluation of the balance due on business combination in Q2 2023, not repeated in 2024 and to the increase in interest and accretion related to the convertible debenture and convertible loan.

During the six-month period ended June 30, 2024, the finance expenses totaled $0.5 million as compared with an income of $1.8 million for the 2023 comparable period, representing a variation of $2.4 million year-over-year. This is due to the favourable revaluation of the balance due on business combination due to two milestones that would not be achieved, thus a reversal of the liabilities was recorded. In addition, greater financial expenses were due to the interest and accretion for the convertible debenture and convertible loan.

7. Strategic Investments

During the three-months ended June 30, 2024, the adjustment to fair market value of strategic investments for Q2, 2024 resulted in a loss of $0.04 million compared to a loss in the amount of $1.2 million in Q2, 2023, a favorable variation of $1.2 million. During the six-months ended June 30, 2024, the adjustment to fair market value of strategic investments resulted in a loss of $0.2 million compared to a loss in the amount of $0.9 million for the same period in the prior year, a favorable variation of $0.7 million. The decrease in loss for the three and six-month periods ended June 30, 2024, is attributable to the variation of the market value of the common shares owned by the Company of HPQ Silicon Inc.

8. Other Income

During the three-months ended June 30, 2024, Other Income includes a gain on settlement of legal proceedings with a third party which was also a customer of the Company’s subsidiary, Pyro Green-Gas. As a result, the Company received a settlement of $1.5 million and recognized a gain of $1,180,335 and the remainder as a reduction of accounts receivable.

9. Comprehensive Income (loss)

The comprehensive income for Q2, 2024 of $1.4 million compared to a loss of $6.3 million, in Q2, 2023, represents a variation of $7.8 million, and is primarily attributable to the factors described above, which have been summarized as follows:

- an increase in product and service-related revenue of $0.9 million arising in Q2, 2024, which generated a 29% gross margin, compared to 37% in Q2 2023. As a result, gross profit is $1.1 million in both the current and comparable three-month period,

- a decrease in SG&A expenses of $6.2 million arising in Q2, 2024, was primarily due to the expected credit loss and bad debt decrease, and also to lower professional fees, other expenses and foreign exchange from the U.S. dollar. This was offset by increases in employee compensation, office and general, depreciation of right-of-use assets, and government grants,

- a decrease in share-based expenses of $0.4 million

- a decrease in R&D expenses of $0.5 million due to a reduction of R&D activities,

- an increase in net finance expenses primarily due to the revaluation of the balance due on business combination in Q2 2023, not repeated in 2024,

- a favourable variation in the fair market value of strategic investments of $1.2 million, and the $1.2 million gain on the legal settlement.

The comprehensive loss for the six-month period ended June 30, 2024, of $3.0 million compared to a loss of $12.5 million, for the same period in the prior year, represents a variation of $9.5 million, and is primarily attributable to the factors described above, which have been summarized as follows:

- an increase in product and service-related revenue of $1.8 million, which generated a 25% gross margin, compared to 29% in 2023. As a result, gross profit is $1.9 million compared to $1.6 million for the same six-month period of 2023,

- a decrease in SG&A expenses of $9.2 million was primarily due to the favourable impact of the expected credit loss and bad debt decrease and also to the decrease in employee compensation, professional fees, travel, depreciation of property and equipment, other expenses and foreign exchange but slightly offset by an increase in office and general, and government grants,

- a decrease in share-based expenses of $1.0 million

- a decrease in R&D expenses of $0.6 million primarily due to decreased R&D activities,

- an increase in net finance expenses primarily due to the revaluation of balance due on business combination of $2.1 million in 2023 not repeated in 2024,

- a favourable variation in the fair market value of strategic investments of $0.7 million, and the $1.2 million gain on the legal settlement.

10. Liquidity and Capital Resources

As at June 30, 2024, the Company had cash of $3.4 million, included in the net working capital deficiency of $9.2 million. Certain working capital items such as billings in excess of costs and profits on uncompleted contracts do not represent a direct outflow of cash. The Company expects that with its cash, liquidity position, and its access to capital markets it will be able to finance its operations for the foreseeable future.

The Company’s term loan balance at June 30, 2024 was $317,140 and decreased by $86,939 since December 31, 2023, due mainly to the complete reimbursement of a loan. The decrease from January 1, 2023, to December 31, 2023 was mainly attributable to the accretion on the Economic Development Agency of Canada loan, which is interest free and will remain so, until the balance is paid over the 60-month period ending March 2029. In July 2023, the Company closed a brokered private placement for $3,030,000, bearing interest at 10%. On December 20, 2023, the Company closed a non-brokered private placement of a convertible loan for gross proceeds of $1,250,000 and bears interest at 3%. The average interest expense on the other term loans and convertible debenture is approximately 10%. The Company does not expect changes to the structure of term loans and convertible debentures and loans in the next twelve-month period. The Company maintained one credit facility which bears interest at a variable rate of prime plus 2%, therefore 7.95% at June 30, 2024. The Company will continue to reimburse the existing credit facility in 2024.

OUTLOOK

Consistent with the Company’s past practice, and in view of the early stage of market adoption of our core lines of business, the Company is not providing specific revenue or net income (loss) guidance for 2024. The following is an outline of the Company’s strategy plus key developments that are expected to impact subsequent quarters.

Overall Strategy

PyroGenesis provides technology solutions to heavy industry that leverage the Company’s expertise in ultra-high temperature processes. The Company has evolved from its early beginnings as a specialty-engineering firm to being a provider of a robust technology eco-system for heavy industry that helps address key strategic goals.

The Company believes its strategy to be timely, as multiple heavy industries are committing to major carbon and waste reduction programs at the same time as many governments are increasingly supportive – from both a policy and financial perspective – of environmental technologies and infrastructure projects. Additionally, both industry and government are developing strategies to ensure the availability of critical minerals during the coming decades of increased output demand.

While there can be no guarantees, the Company believes the evolution of its strategy beyond greenhouse gas emission reduction, to an expanded focus that encapsulates the key verticals listed in the section “Q4 2024 Production and Sales Highlights”, both (i) improves the Company’s chances for success while (ii) also providing a clearer picture of how the Company’s wide array of offerings work in tandem to support heavy industry goals.

PyroGenesis’ market opportunity is significant, as major industries such as aluminum, steelmaking, manufacturing, cement, chemicals, defense, aeronautics, and government seek factory-ready, technology-based solutions to help steer through the paradoxical landscape of increasing demand, tightening regulations, and material availability.

As more of the Company’s offerings reach full commercialization, PyroGenesis will remain focused on attracting influential customers in broad markets while at the same time ensuring that operating expenses are controlled to achieve profitable growth.

Cost Controls and Efficiencies

PyroGenesis has been, and continues to, scrutinize both potential and existing projects to ensure that the utilization of labour and financial resources are optimized. The Company continues to only engage in projects that reflect significant benefits to PyroGenesis and the risks of which are defined. The Company intends to intensify its focus on project and budgetary clarity during this period of elevated inflationary pressures, by identifying alternative suppliers while constantly adjusting project resources. The early-stage project assessment process has also been refined to allow for a faster “go / no-go” decision on project viability.

Enhanced Sales and Marketing

Against the backdrop of this 3-tiered strategy, the Company continues to increase sales, marketing, and R&D efforts in-line with – and in some cases ahead of – the growth curve for industrial change related to greenhouse gas reduction efforts.

Initiatives during the second quarter 2024 included enhanced use of video, including a long form video message from the Company’s CEO as part of the Company’s annual general meeting.

Macroeconomic Conditions

With some continued uncertainty in the macroeconomic environment, including ambiguity in the banking sector with regard to interest rate adjustments, and the continued inflationary pressures causing shifting demand dynamics across various industries at different times, it may be difficult to assess the future impact these events and conditions will have on our customer base, the end markets we serve and the resulting effect on our business and operations, both in the short term and in the long term.

Despite these uncertainties, we continue to believe there is an accelerated need for PyroGenesis’ solutions in the industries we serve as heavy industry continues to decarbonize / transition their energy sources, manufacture utilizing both lighter metals (such as aluminum) and additive manufacturing techniques, and deal with tighter hazardous waste regulations.

While we expect these uncertainties and other macroeconomic conditions to continue to impact the variability in our quarter to quarter revenue, we believe our diversity in both customer base and solution set will continue to be a strong mitigating factor to these challenges. Additionally, the Company’s ongoing efforts to reduce costs through various measures including the sourcing of more high quality, cost-competitive suppliers, further bolsters the Company against cost fluctuations.

The various military conflicts in the Middle East and Eastern Europe continue to create some level of global economic uncertainty, as well as supply chain disruptions that can change at any time. However, it’s important to note that the Company does not have any operations, customers or supplier relationships in Russia, Belarus or Ukraine, and as such are not directly impacted at a customer level in these countries. The Company does have customer relationships and projects in Poland and will continue to monitor the situation in the region regarding challenges to the completion of current projects, which at this time are not inhibited.

As always, the Company monitors the potential impact macroeconomic events and conditions could have on the business, operations, and financial health of the Company.

Generally, the Company believes that broad-based threats to global supply chains increase awareness and interest in the many solutions the Company offers. This is particularly true within the minerals and metals industries, as manufacturers seek alternatives to off-shore suppliers as well as technologies that could optimize output or recycle critical material from byproducts or waste – solutions that the Company currently offers.

Business Line Developments

The upcoming milestones which are expected to confirm the validity of our strategies are outlined below (please note that these timelines are estimates based on information provided to us by the clients/potential clients, and while we do our best to be accurate, timelines can and will shift, due to protracted negotiations, client technical and resource challenges, or other unexpected situations beyond our or the clients’ control):

Business Line Developments: Near Term (0 – 3 months)

Financial

- Payments for Outstanding Major Receivables:

Regarding the outstanding receivable under the Company’s existing $25 million+ Drosrite™ contract: as previously announced, PyroGenesis had agreed to a strategic extension of the payment plan, by the customer and its end-customer, geared to better align the pressures on the end-user’s operating cash flows created by increased business opportunities. In Q2 2024, the Company received a planned payment in the amount of $4.1 million. Another portion of the balance is expected to be paid in the near term.

- Warrant repricing:

Post quarter end, in July 2024 [news release dated July 03, 2024], the Company announced that up to 4,107,850 common share purchase warrants will be amended such that the exercise price would be reduced to $0.75 per share provided that if the closing price of the common shares exceeds $0.9375 (such amount being 125% of $0.75) over any 5 consecutive trading days, the Company will be entitled to accelerate the expiry date of the warrants to the date that is 30 days following the date that notice of such acceleration is provided.

Energy Transition & Emission Reduction

- Aluminum Remelting Furnaces:

As mentioned in the Q1 2024 Outlook, the Company has been working on aluminum remelting furnace solutions using plasma, for use by secondary aluminum producers or any manufacturer of aluminum components that uses recycled or scrap aluminum. With gas-fired furnaces responsible for much of the scope 1 emissions of secondary aluminum production, aluminum companies have been searching for solutions that can help in the decarbonization efforts of aluminum remelting and cast houses.

The Company has two concepts: the retro-fitting of plasma torches in existing remelting and cast house furnaces that currently use other forms of heating, such as natural gas; and the manufacturing and sale of a PyroGenesis produced furnace based off the Company’s existing Drosrite metal recovery furnace design, which has been in use commercially for several years.

Also as mentioned in previous Outlooks, the Company has been working with different companies over the past few years towards these goals. During Q2 2024, the Company announced a signed letter of intent with global aluminum product manufacturer Constellium for large-scale plasma remelting furnaces, and a contract with a global mining supply company, with the agreement related to the client’s intention to examine the use of plasma in decarbonizing its cast houses. Discussions remain underway with other clients for similar contracts.

- Aluminum Furnace Tests:

The Company has started, and will continue in the near term, live furnace tests of plasma as a process heat source in melting and holding furnaces with major aluminum companies, and is in advanced discussions with other companies for similar live furnace tests of plasma as a process heat source in melting and holding furnaces. Due to the nature of these tests and the increasing number of similar tests, the Company may choose not to announce every test session it engages in.

- New Industry Contract for Plasma Torches:

As noted in the Q1 2024 Production and Sales Highlights, in January 2024, the Company announced the signing of a framework master agreement with a client (whose name is being withheld for confidentiality and competitive reasons), which included the payment to the Company of a non-refundable downpayment for $667,000. As stated in the Q4 2023 Outlook, this marks PyroGenesis’ resumption of work in an industry that previously showed promise.

Negotiations of a first substantial statement of work are ongoing and remain positive but depend in large part on the client’s ability to secure funding in a timely manner. The client now anticipates proceeding with the purchase of a single plasma torch system in the near term, followed by one or more larger orders in subsequent quarters, dependent upon the client’s financing. While there is no guarantee this statement of work or additional ones will be completed, if successful the Company foresees the potential for a multi-phase, multi-year partnership with the client that may result in many additional plasma torch orders over the next few years.

- Iron Ore Pelletization Torch Trials:

As mentioned in previous Outlooks, the commissioning of the plasma torch systems – for use in the pelletization furnaces of a client previously identified as Client B – was underway, with the Company’s engineers onsite at Client B’s iron ore facility. The commissioning process includes installation, start-up, and site acceptance testing (SAT). The Company previously announced that it had shipped four 1 MW plasma torch systems for use in Client B’s iron ore pelletization furnaces, for trials toward potentially replacing fossil-fuel burners with plasma torches in Client B’s furnaces.

As mentioned in previous Outlooks, this project continues to move forward, however the commissioning suffered a series of unforeseeable delays caused by, among other things, damaging regional torrential rainstorms that flooded and damaged the facility’s electrical system and furnace components, and intermittent power outages that led to damage of the plasma burners cooling system.

Client B remains committed to the trials and additional process steps are being designed to account for the client’s particular mechanical and environmental risk variables.

The client previously identified as Client A, a large international mining company which has also purchased a full plasma torch system for use in trials in its pelletization furnaces, continues its plasma torch initiative at its own pace, with no recent developments to report as per project timing or completion.

- Aluminum Cast House Decarbonization:

The Company is part of a tendered bid process for the testing of plasma within an aluminum cast house of a leading global aluminum company. This is unrelated to the project announcement made in conjunction with Constellium. During the quarter, the Company was advanced past the preliminary tender phase to the full tender proposal phase.

The Company’s full proposal is now due in August, with the final client decision expected in the near-to mid-term.

- Mining Industry Parts Manufacturer Decarbonization:

As noted above, in April 2024 the Company announced the signing of a contract with a client to assess the applicability and examine the use of plasma as a heat source in the client’s cast furnaces. The client, a billion-dollar entity with facilities on five continents, is one of the world’s largest manufacturers of products that serve the mining and defense industries, amongst others.

The tests noted as targeted for completion by the end of the Q2 were conducted and have concluded, successfully.

Negotiations are now underway for the sale of initial plasma torch system(s) as well as the accompanying manipulation/handling components, as a per unit price of between US$500,000-$1,000,000 in revenues to PyroGenesis per torch.

Commodity Security & Optimization

- “FSR” Project:

Post quarter end, in July, the Company’s client, HPQ Silicon Inc., announced [news release dated July 30th] the start of commissioning of the Fumed Silica Reactor (FSR) pilot plant (described above in greater detail in the “Q2 2024 Operational Highlights” section).

The pilot plant will commence pre-commercial sample batches of fumed silica in the near term.

- Plasma-Based Graphite Production:

The Company is in advanced discussions with an entity engaged in the production of graphite, for a first phase design and delivery of a customized pilot-scale plasma reactor and associated testing system, with an estimated value of between $500,000 to $1 million.

- Drosrite Factory Trials:

The Company is in final logistical discussions with multiple aluminum manufacturers regarding on-site trials of the Company’s Drosrite furnace system for the processing of aluminum dross, as a first step towards potential purchase of Drosrite systems. These particular potential clients are located across Europe and the United States.

- Titanium Metal Powder

As noted above in the Q2 2024 Production and Sales Highlights, in June the Company announced that it had cleared the final requirement to becoming an approved supplier of its titanium metal powder to a global aerospace original equipment manufacturer.

The formal process for adding the Company to the approved supplier list has begun and is expected to be complete in the near term.

Waste Remediation

- SPARC Refrigerant Waste Destruction System:

The Company is in negotiations with a large US-based distributor of refrigerants and specialty gases for the construction of the Company’s SPARC (Steam Plasma Refrigerant Cracking) system, for the safe destruction of hazardous end-of-life refrigerants, such as CFCs, HCFCs, and HFCs, for a contract amount of approximately $2-3 million.

- Plasma-Based Glass Valorization:

The Company is in final negotiations with an entity in Canada, for a plasma-based furnace for use in the melting and valorization of recycled glass.

Business Line Developments: Mid Term (3-6 months)

Energy Transition & Emission Reduction

- Plasma Torch Systems:

The Company has been negotiating with a North American entity for the sale of a hyper power level plasma torch system of between 15-25MW, with a potential contract value of between $15-25 million.

Commodity Security & Optimization

- Drosrite Systems:

The Company is in various stages of discussions with aluminum manufacturers to purchase Drosrite aluminum dross processing systems, including with two Middle Eastern aluminum companies for the purchase of multiple 5,000+ tonnes per year Drosrite furnaces.

- Titanium Metal Powder:

The Company is in discussions with several companies about possible contracts for both fine and coarse cut titanium metal powder. These include large European and North American firms within the aerospace and materials supply industries.

Business Line Developments: Long Term (> 6 months)

Commodity Security & Optimization

- Plasma Resource Recovery System (PRRS):

Post quarter end, the Company announced [news release dated July 29, 2024] the signing of a contract for a land-based waste-to-energy system to a European entity, to transform municipal solid waste into both energy and chemical products. The contract was announced as two phased: phase 1 is a signed $2 million contract for a conceptual and preliminary design phase; phase 2 is the construction and delivery of a final system. Phase 1 is expected to be completed in 2025. Phase 2 is dependent on the client obtaining the required financing and the negotiation of terms and conditions. As noted in the news release, the potential value for this contract grew from approximately $25-$30 million to between $120-160 million, with final decision based on the results of the phase one project, which is scheduled for completion in Q3 2025.

Separately, the Company is in initial discussions with an additional European company for the Company’s Plasma Resource Recovery System, for use in the pyrolysis of plastics.

Waste Remediation

- Plasma Torches:

The Company has been in discussions over several years with a European entity, to act as a potential supplier of plasma torches for the entity’s waste-to-energy initiatives; the entity has, at times, listed PyroGenesis as their torch supplier in various publications online. This entity has recently announced having entered into an agreement with a German multi-Billion-dollar leading technology company to accelerate green energy transition through waste-to-energy technology. The entity announced that it aims to establish 300 plants producing 1 million tons of hydrogen over the next several years.

** Please note that projects or potential projects previously announced that do not appear in the above summary update should not be considered as at risk. Noteworthy developments can occur at any time based on project stages, and the information presented above reflects information on hand. Projects not mentioned may have simply not concluded or not presented milestones or client updates worthy of discussion or update.

FURTHER INFORMATION

Additional information relating to Company and its business, including the 2023 consolidated financial statements, the Annual Information Form and other filings that the Company has made and may make in the future with applicable securities authorities, may be found on or through SEDAR+ at www.sedarplus.ca, or the Company’s website at www.pyrogenesis.com.

Additional information, including directors’ and officers’ remuneration and indebtedness, principal holders of the Company’s securities and securities authorized for issuance under equity compensation plans, is also contained in the Company’s most recent management information circular for the most recent annual meeting of shareholders of the Company.

About PyroGenesis Canada Inc.

PyroGenesis Canada Inc., a high-tech company, is a leader in the design, development, manufacture and commercialization of advanced plasma processes and sustainable solutions which reduce greenhouse gases (GHG) and are economically attractive alternatives to conventional “dirty” processes. PyroGenesis has created proprietary, patented and advanced plasma technologies that are being vetted and adopted by multiple multibillion dollar industry leaders in four massive markets: iron ore pelletization, aluminum, waste management, and additive manufacturing. With a team of experienced engineers, scientists and technicians working out of its Montreal office, and its 3,800 m2 and 2,940 m2 manufacturing facilities, PyroGenesis maintains its competitive advantage by remaining at the forefront of technology development and commercialization. The operations are ISO 9001:2015 and AS9100D certified, having been ISO certified since 1997. For more information, please visit: www.pyrogenesis.com.

This press release contains “forward-looking information” and “forward-looking statements” (collectively, “forward-looking statements”) within the meaning of applicable securities laws. In some cases, but not necessarily in all cases, forward-looking statements can be identified by the use of forward-looking terminology such as “plans”, “targets”, “expects” or “does not expect”, “is expected”, “an opportunity exists”, “is positioned”, “estimates”, “intends”, “assumes”, “anticipates” or “does not anticipate” or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might”, “will” or “will be taken”, “occur” or “be achieved”. In addition, any statements that refer to expectations, projections or other characterizations of future events or circumstances contain forward-looking statements. Forward-looking statements are not historical facts, nor guarantees or assurances of future performance but instead represent management’s current beliefs, expectations, estimates and projections regarding future events and operating performance.

Forward-looking statements are necessarily based on a number of opinions, assumptions and estimates that, while considered reasonable by the Company as of the date of this release, are subject to inherent uncertainties, risks and changes in circumstances that may differ materially from those contemplated by the forward-looking statements. Important factors that could cause actual results to differ, possibly materially, from those indicated by the forward-looking statements include, but are not limited to, the risk factors identified under “Risk Factors” in the Company’s latest annual information form, and in other periodic filings that the Company has made and may make in the future with the securities commissions or similar regulatory authorities, all of which are available under the Company’s profile on SEDAR+ at www.sedarplus.ca. These factors are not intended to represent a complete list of the factors that could affect the Company. However, such risk factors should be considered carefully. There can be no assurance that such estimates and assumptions will prove to be correct. You should not place undue reliance on forward-looking statements, which speak only as of the date of this release. The Company undertakes no obligation to publicly update or revise any forward-looking statement, except as required by applicable securities laws.

Neither the Toronto Stock Exchange, its Regulation Services Provider (as that term is defined in the policies of the Toronto Stock Exchange) nor the OTCQX Best Market accepts responsibility for the adequacy or accuracy of this press release.

For further information please contact:

Rodayna Kafal, Vice President, IR/Comms. and Strategic BD

E-mail: ir@pyrogenesis.com

RELATED LINK: http://www.pyrogenesis.com/

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/4560d4c2-3dac-4843-98a9-6b9f9f35dc93